US Shale Production Revisited

US Shale Production Revisited

Or why the Permian is scaring me.

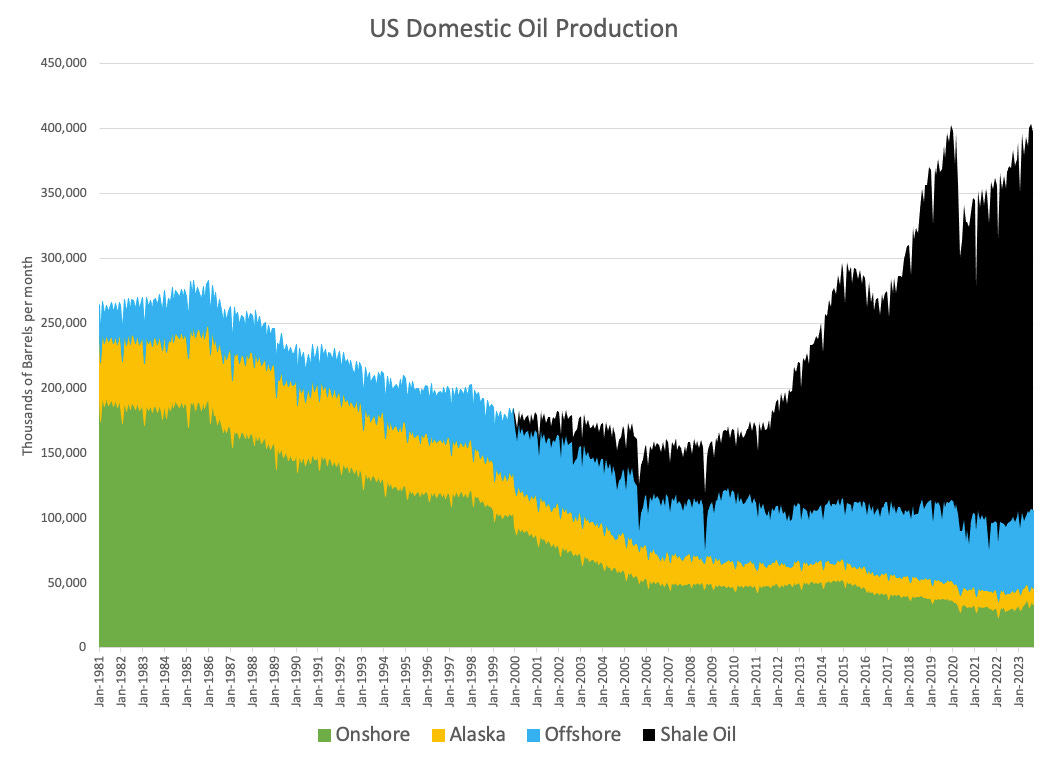

Since 2012, US oil and natural gas production has been dominated by shale.

And shale has been dominated by the Permian. Between January 2021 and January 2024, shale oil production grew by 1.63 million barrels per day and 1.54 million barrels (94%) of that increase came from the Permian. And while the Permian is thought of as an oil field, it accounted for 49% of the 15.5 billion cubic feet per day natural gas production growth over the same time frame. Producing almost 25 billion cubic feet per day, the Permian is almost 25% of US domestic gas production.

But there are beginning to be troubling signals that the Shale Revolution and specifically the Permian may be reaching their limit.

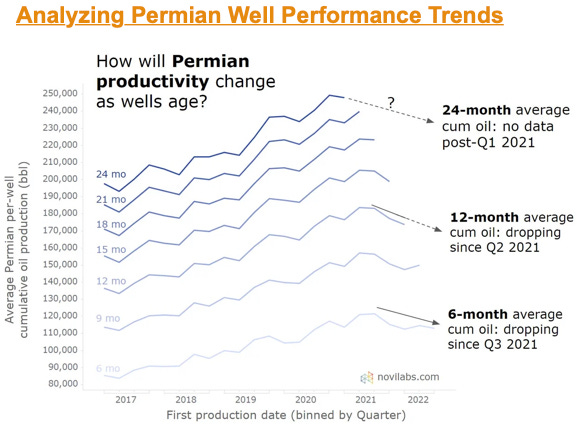

Let’s start with this graphic from NoviLabs where they measure the cumulative production from Permian oil wells.

First thing to notice is that the cumulative production for wells drilled after 2021 is less than the wells drilled in 2021. Prior to 2021, cumulative production had been improving as horizontal wells became longer and fracking techniques improved. But since 2021, the 6 month cumulative has tapered off slightly.

Why is that important? If you look, the chart starts at 80,000 barrels rather than zero, that means that a Permian shale oil well makes almost 50% of it’s two-year production in the first six months. So, those first six months are extremely indicative of what the cumulative production for the life of the well is going to be. We are also starting to see some decline in the 9-month and 12-month curves.

A key point to understand is that existing wells are in decline. Every month existing production declines and new wells are needed just to keep production rates flat.

Energy Information Agency (eia.gov)- https://www.eia.gov/petroleum/drilling/pdf/permian.pdf April 2024

The Energy Information Agency of DOE is estimating that for April 2024, 315 drilling rigs in the Permian will add enough new wells to produce 437,000 barrels per day, but that existing wells will decline in production by 425,000 barrels per day, resulting in those 315 rigs only increasing overall production by 12,000 barrels per day. This is the "Red Queen Effect" mentioned by Ted Cross of NoviLabs in posts on LinkedIn and Twitter : "It takes all the running you can do, to keep in the same place." A reference to the Red Queen in Lewis Carroll’s Through the Looking Glass.

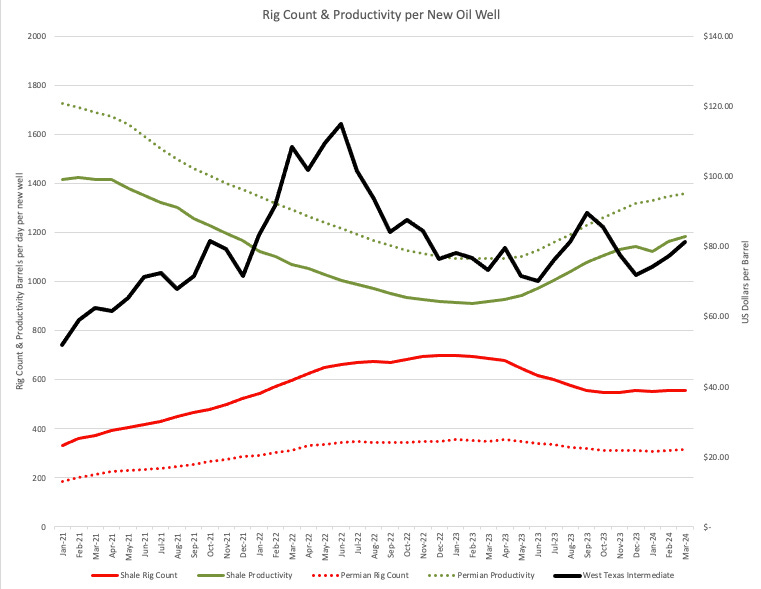

Looking at production per well, rig count, and oil prices we can see that high prices in 2022 spurred an increase in active rigs, but a decline in productivity. This is indicative that at these higher prices, oil companies were willing to develop some of their lesser quality acreage and this dragged down the productivity.

Author’s analysis of EIA.gov Drilling Productivity Data for Shale Fields.

When oil prices declined in late 2022 through 2023, the oil companies decreased the number of rigs and went back to focusing on the more productive acreage, causing productivity to increase.

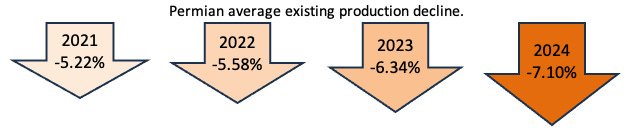

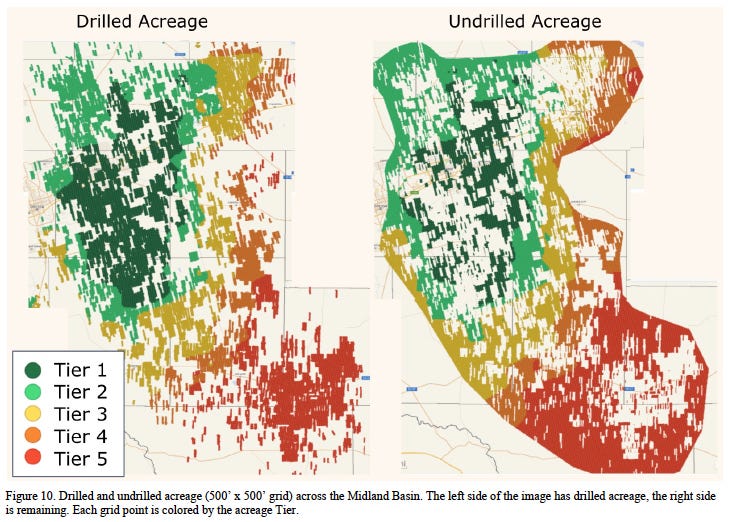

This goes back to the previous post on proven reserves (Proven, Probable, and Possible), not all acreage is created equally, some is better than others. The convention is to rank acreage as tier 1 through tier 5, with 1 being the best quality acreage. And once you have used up all the best tier 1 acreage, then we would expect to see well productivity to begin to decline.

And we are seeing that. The decline rate has increased since 2021 as more lower tier acreage was developed in 2022 and 2023. This runs counter to the argument that Ted Cross was making about the Red Queen effect. His theory was that as more production comes from older wells, then production should be more stable. But the problem is that as more production comes from tier 3, 4, and 5 acreage, decline rates will increase. Meaning we will have to run even faster to stay in place.

And that is the indication we are now getting from the Permian. In a 2022 paper released by NoviLabs, they indicated that 61% of the tier 1 acreage in the Midland basin had been developed.

When the Music Stops: Quantifying Inventory Exhaustion in the Midland Basin with Machine Learning - T. Cross, J. Reed, K. Long (Novi Labs). Copyright 2022, Unconventional Resources Technology Conference (URTeC) DOI 10.15530/urtec-2022-3722909

When I followed up with them for an update, their indication was “…There is only ~1.6 years of remaining inventory that breaks even under $50/bbl (tier 1) and over nine years remaining that breaks even under $80/bbl…”

This is the very early days of these indicators and we could see improvements. But if we don’t see some turnaround in these numbers then we have to be cognizant that the Permian could be plateauing.

What does that mean? It means higher oil prices for one thing. Less productivity per well, means you need to drill more wells to keep production rates steady and that will mean higher drilling costs, which can only be justified with higher oil prices. It also means that America's energy independence will come to an end.

The potential for oil imports may not upset people. After all we went through the same thing already. Once US domestic production peaked in 1973, we saw an increase in oil imports.

On the natural gas side, it should be much more concerning. The US has enjoyed very cheap natural gas prices that has allowed the electricity market to shift from coal fired power plants to natural gas with a corresponding decrease in CO2 emissions. A decreasing domestic natural gas production means one of three things -

Start importing natural gas which will tie the US market to the worldwide LNG market and drive up natural gas prices and electricity costs.

Switch back to coal which will drive up CO2 emissions and drive up electricity costs.

Build more renewables, which while cheap, increases volatility in the electricity markets unless large energy storage systems are built. And energy storage makes the grid more stable, but is expensive, which makes renewables more expensive.

You will note, all three scenarios increase the cost of electricity. Add in the growth in data centers due to AI and cryptocurrency, toss in more electrification as higher gasoline and natural gas prices drive consumers to EVs, heat pumps, and induction cooking, and you have all the ingredients for an energy shortage. A energy transition not driven by climate change, but by basic petroleum engineering that dictates that all oil fields plateau and eventually go into decline.

This is my concern. Some analysts show US domestic production increasing in the future driven by increasing demand, but they don’t show where it is coming from and with Permian and other big shale fields showing signs of plateauing I don’t see where they are going to get it. The undeveloped and lesser developed shale fields are all smaller than the seven major fields we rely upon so replacing the big seven is just not feasible.

This is the classic problem of people looking at tomorrow, but no one is planning for twenty years down the road.

And that is one of the key points in my book - “Fixing America - An Engineer’s Solution to our Social, Cultural, and Political Problems. If you are interested in the book, this button will link you to where you can find it.